By David Lawrence

Rwanda has one of the world’s fastest-growing economies, driven by economic and structural reforms and strong international support. Growth averaged 7.5 percent annually in the decade to 2018. The government has even higher goals through its National Strategy for Transformation and Vision 2050 strategy: to reach middle-income status in 15 years. That will require an economic shift toward high-value, competitive sectors, particularly those that could generate exports. It also will depend on better regional economic integration through the East African Community (EAC) and access to ports through Kenya and Tanzania.

But Rwanda—with private sector participation—can drive one area of growth: housing, which does not depend on export markets. Demand for secure, affordable housing is surging because of fast urban population growth—estimated at 5.75 percent annually, more than twice the rate of overall population growth in the country. By comparison, World Bank data shows that urban population growth globally in 2018 was 1.93 percent, nearly twice the rate of overall global population growth of 1.1 percent.

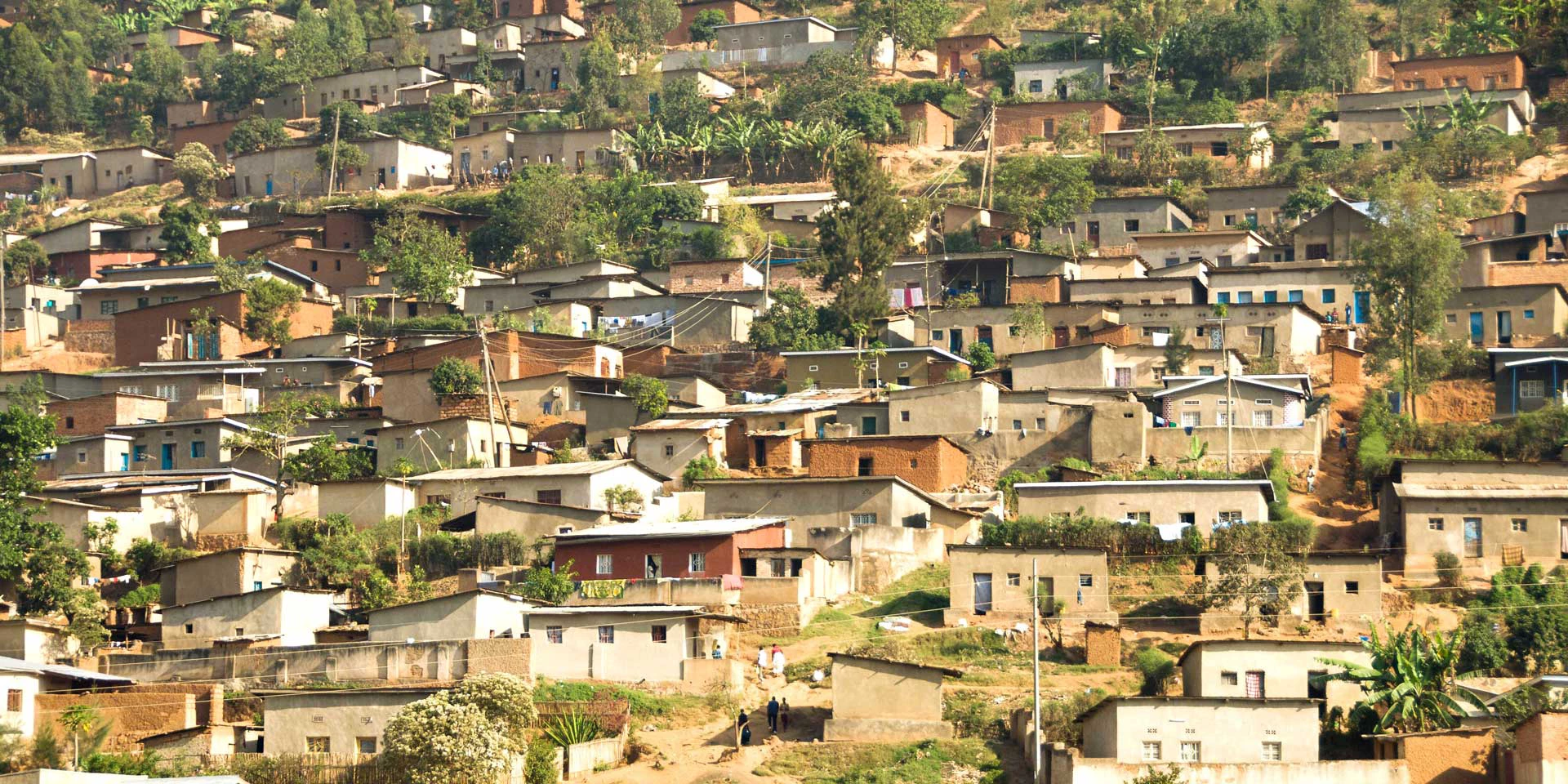

In Kigali alone, demand for new houses over the next three years is projected at nearly 350,000, with the current pace of only 1,000 housing units built per year illustrating a widening gap. Secondary cities—Huye, Muhanga, Musanze, Nyagatare, Rubavu, and Rusizi—also face significant housing deficits. And new homes are affordable for only the top 20 percent of the population.

For most people in the affordable housing segment—which the government defines as those with monthly incomes below $232—formal housing is out of reach. “There is a huge gap in the housing sector that is underserved,” said Dan Kasirye, IFC’s Resident Representative based in Kigali. “It is definitely a sector with huge potential.”

Demand for new houses in Kigali will reach 350,000 units over the next three years. © Black Sheep Media/Shutterstock.com

The World Bank Group’s Rwanda Country Private Sector Diagnostic (CPSD), published earlier this year, identified affordable housing as a sector with significant potential for economic growth, job creation, and development impact in the next three to five years. Attracting private sector participation will require a multi-faceted approach that is a top priority for the reform-minded government. Analysts believe that private sector firms such as construction companies, developers, building materials producers, and firms offering professional services (for example, architects) could take advantage of new opportunities in the affordable housing sector.

Charles Haba, managing director of Century Real Estate in Kigali, is cautiously optimistic. “The housing market in Rwanda is largely untapped, and one has to be cautious about how to approach it,” he said. “There is huge potential in the middle to high-end of the market. To make money in the lower end, you need to have scale. But overall, I would say aspirations for the housing market are ascending.”

An Opening for International Developers

The private sector diagnostic argues that establishing incentives to attract international developers capable of undertaking large-scale housing projects could stimulate private sector investment and diversification in the affordable housing sector. A targeted incentive framework could include import tax rebates, fee waivers, serviced land mechanisms, or innovative financing methods, the report said.

It also suggests ways to overcome the shortage of professionals who are essential for delivering housing at scale, such as architects, engineers, and developers. Building the necessary financial, city management, administrative, and technical capacity is seen as essential for implementing developmental plans. Vocational training and expanded tertiary education programs could supply the necessary skills. Programs to bring in regional and international talent to meet local demand may also be an option.

Supporting the banking sector is also key to help improve housing affordability—by making cheaper mortgage loans available to more Rwandans. Today, fewer than 5 percent of Rwandans use bank credit to purchase a home. Mortgages target the formally employed, which excludes a large proportion of the population—fewer than 1 percent of Rwanda’s households today can afford a $40,000 house through a mortgage. Furthermore, financial institutions do not have the resources or capacity to provide long-term financing—most banks rely on short-term deposits, which limits their ability to offer long-term housing loans.

Public-private partnerships could help develop urban infrastructure—a current challenge to the housing sector. © Shutterstock.com

But an effort is underway to expand the mortgage financing market. The World Bank and IFC are collaborating on the Rwanda Affordable Housing Finance Project to establish and support the Rwanda Mortgage Refinance Company, which would enable the banking sector to provide mortgage financing. The World Bank is providing a $150 million, 25-year credit facility through the project, which will be part of a revolving fund that can provide affordable mortgage loans to Rwandans below commercial bank ranks, and with longer repayment periods. A potential IFC investment in collaboration with the Rwanda Social Security Board could enable the construction of over 2,000 units of moderately priced housing. IFC support for public-private partnerships, such as the PPP framework study undertaken by Deloitte, could benefit the sector by addressing infrastructure issues.

The potential size of the housing market in Rwanda is not as large as it is in Kenya or South Africa, both of which have much larger populations and economies. But government commitment—through the provision of land, support for local infrastructure, tax incentives, and willingness to provide debt and equity through sovereign investment entities—makes projects in Rwanda’s housing sector attractive to local and international investors, according to analysts.

In addition to the Rwanda Social Security Board, key government bodies such as the Rwanda Housing Authority, the Ministry of Finance, and the Ministry of Infrastructure—with active support from Rwandan President Paul Kagame —have pledged to work with industry players to facilitate investments in affordable housing. As a result, prospects look promising.

“While there are still challenges, we believe the market will be ready for investments,” said Olaf Schmidt, an IFC Manager based in Johannesburg, an IFC regional hub.